import os

os.chdir(r"D:\github\dslian\body")17 ARMA 模型

17.1 \(AR(p)\) 模型

在时间序列分析中,\(AR(p)\) 模型是最基本的模型之一。它假设当前值与过去 \(p\) 个时刻的值存在线性关系。一般形式为:

\[ X_t = \phi_1 X_{t-1} + \phi_2 X_{t-2} + ... + \phi_p X_{t-p} + \epsilon_t \tag{1} \]

其中,\(\phi_1, \phi_2, ..., \phi_p\) 是模型参数,\(\epsilon_t\) 是白噪声项。

17.1.1 \(AR(1)\) 模型

当 \(p=1\) 时,\(AR(1)\) 模型为:

\[ X_t = \phi_1 X_{t-1} + \epsilon_t \tag{2} \]

虽然看起来很简单,但 \(AR(1)\) 模型在时间序列分析中非常重要,因为它可以捕捉到数据的自相关性。从模型设定形式上来看,它具有递推的特征,当前值仅与前一个值相关。

具体而言,(2) 式在 \(t-1\) 时刻可以表示为:

\[ X_{t-1} = \phi_1 X_{t-2} + \epsilon_{t-1} \tag{3} \]

将 (3) 式代入 (2) 式中,我们可以得到:

\[ X_t = \phi_1 (\phi_1 X_{t-2} + \epsilon_{t-1}) + \epsilon_t = \phi_1^2 X_{t-2} + \phi_1 \epsilon_{t-1} + \epsilon_t \tag{4} \]

将 (4) 式继续递推下去,我们可以得到:

\[ X_t = \phi_1^t X_0 + \sum_{i=0}^{t-1} \phi_1^i \epsilon_{t-i} \tag{5} \]

由 (5) 式可知,\(X_t\) 由初始值 \(X_0\) 和过去的随机扰动项 \(\epsilon_{t-i}\) 线性组合而成。

由此,我们可以看出 \(AR(1)\) 模型的一个重要特性:当前值 \(X_t\) 不仅与前一个值 \(X_{t-1}\) 相关,还与更早的值 \(X_{t-2}, X_{t-3}, ...\) 相关。具体来说,当前值 \(X_t\) 是过去所有随机扰动项 \(\epsilon_{t-i}\) 的加权和,其中权重由 \(\phi_1^i\) 决定。随着 \(i\) 的增大,权重 \(\phi_1^i\) 会迅速减小,这表明较早的随机扰动对当前值的影响逐渐减弱。

因此,\(AR(1)\) 模型可以看作是一个具有指数衰减特性的模型。也就是说,当前值 \(X_t\) 主要受到最近的随机扰动项 \(\epsilon_{t-1}\) 的影响,而对更早的随机扰动项的影响则逐渐减弱。这种特性使得 \(AR(1)\) 模型在建模时间序列数据时非常实用,因为它能够有效地捕捉到数据的自相关性和记忆效应。

在实际应用中,\(AR(1)\) 模型常用于建模具有自相关性的时间序列数据,如股票价格、气温等。通过估计参数 \(\phi_1\),我们可以了解数据的自相关程度,从而为后续的预测和分析提供依据。

17.1.2 单位根过程

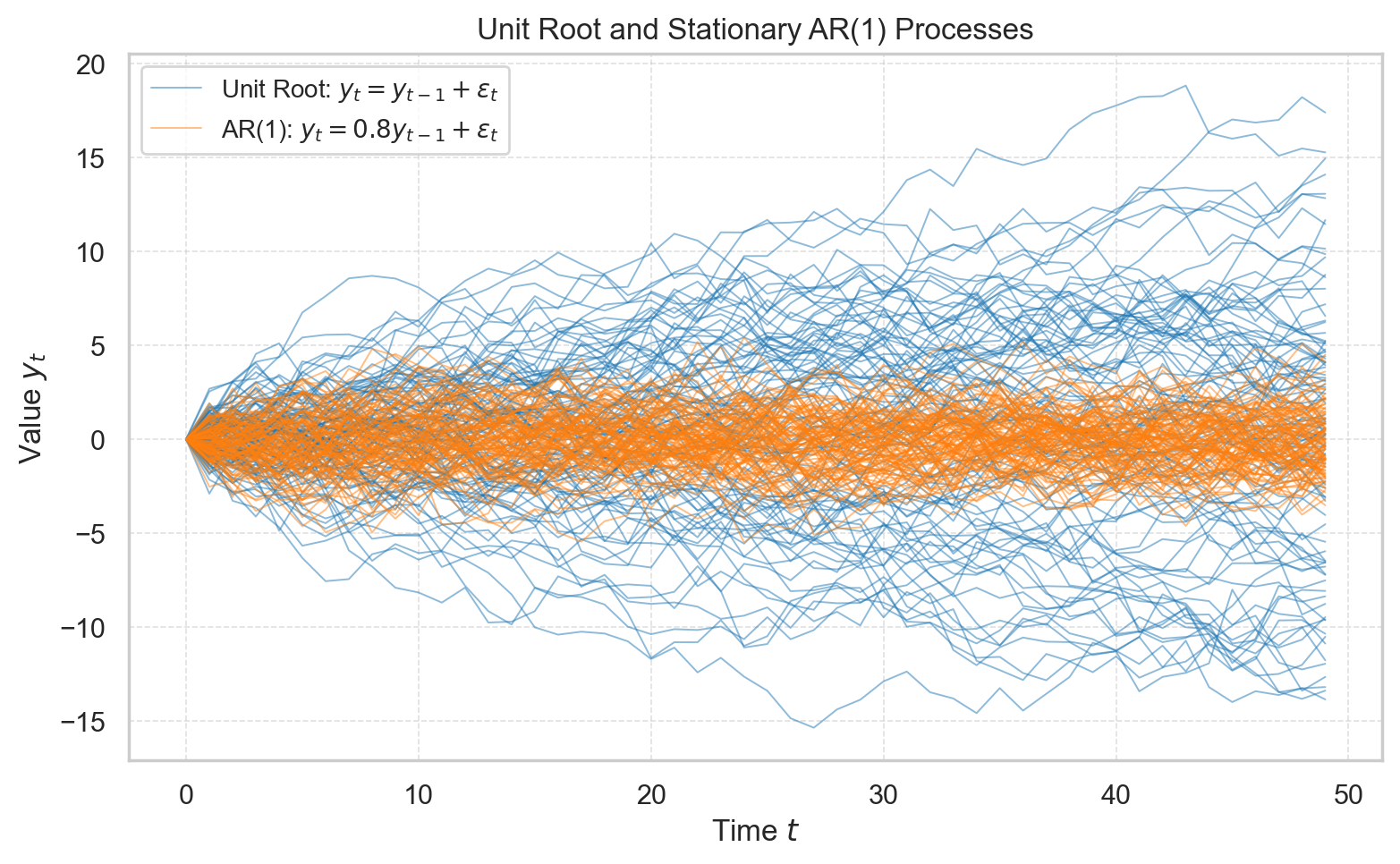

前面已经提到,只有当 \(|\phi_1|<1\) 时,\(AR(1)\) 模型才是平稳的。平稳性是时间序列分析中的一个重要概念,它意味着序列的统计特性(如均值、方差和自相关函数)在时间上保持不变。平稳序列的均值和方差是有限的,并且自相关函数仅依赖于时间间隔,而与具体时间点无关。

那么,当 \(|\phi_1|=1\) 时,\(AR(1)\) 模型会发生什么呢?在这种情况下,模型变为:

\[ X_t = X_{t-1} + \epsilon_t \tag{6} \]

我们称这种模型为单位根过程。单位根过程是一种特殊的非平稳序列,其均值和方差随时间变化而变化。具体来说,单位根过程的均值是无限的,而方差是无穷大的。这意味着单位根过程具有非常强的记忆效应,过去的随机扰动对当前值的影响不会随着时间的推移而减弱。

我们可以将 \(\phi_1 = 1\) 带入 (5) 式中,得到:

\[ x_t = X_0 + \sum_{i=0}^{t-1} \epsilon_{t-i} \tag{5} \]

可见,过往的随机扰动项 \(\epsilon_{t-i}\) 对当前值 \(X_t\) 的影响具有累积性,且它们的影响不会随着时间的推移而减弱。这种特性使得单位根过程具有非常强的记忆效应。用大白话来说,它很记仇,即使是 30 年前受到的冲击,它今天仍然记忆犹新。

具体而言,单位根过程的均值和方差可以表示为:

\[ \mu_t = E[X_t] = E[X_{t-1}] + E[\epsilon_t] = \mu_{t-1} + 0 = \mu_0 \tag{7} \]

\[ \sigma^2_t = Var[X_t] = Var[X_{t-1}] + Var[\epsilon_t] = \sigma^2_{t-1} + \sigma^2_\epsilon = \sigma^2_0 + t \cdot \sigma^2_\epsilon \tag{8} \]

17.1.3 AR 过程与单位根过程的区别

AR 过程和单位根过程的主要区别在于平稳性。AR 过程是平稳的,而单位根过程是非平稳的。平稳性意味着序列的统计特性在时间上保持不变,而非平稳性则意味着序列的统计特性随时间变化而变化。

平稳序列的均值和方差是有限的,并且自相关函数仅依赖于时间间隔,而与具体时间点无关。非平稳序列的均值和方差是无限的,并且自相关函数依赖于具体时间点。

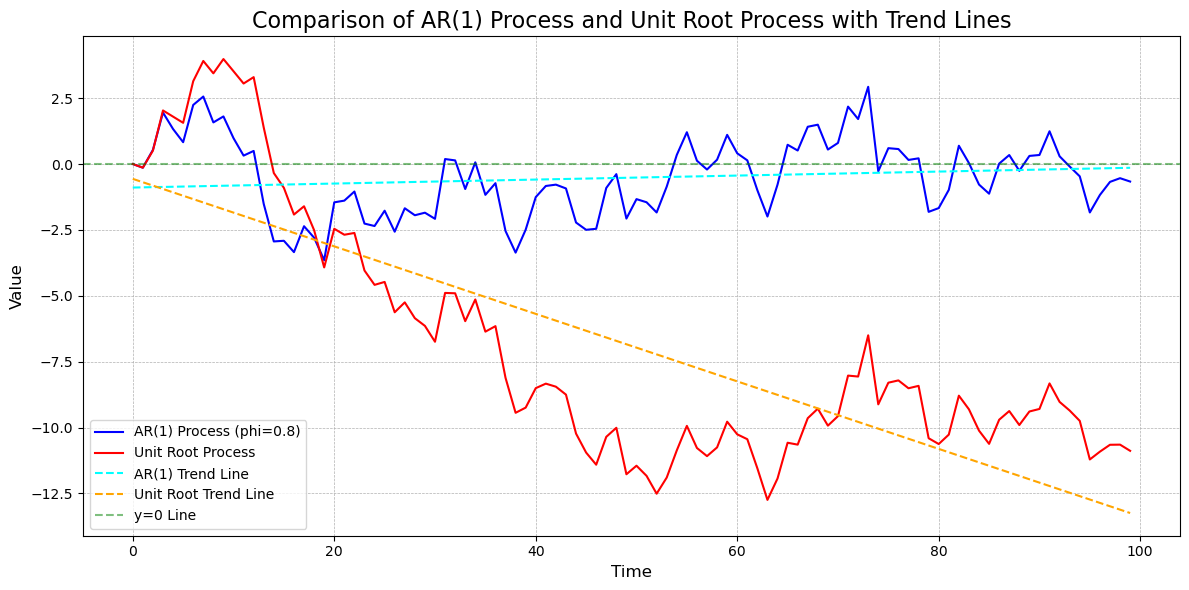

下面,我们通过一个简单的模拟实例来说明 AR 过程和单位根过程的区别。

# 模拟分析平稳 AR(1) 过程与单位根过程的差别

import numpy as np

import matplotlib.pyplot as plt

# 设置随机种子以保证结果可重复

np.random.seed(42)

# 模拟 AR(1) 过程 --------- 参数设定 -----------

n = 100 # 时间序列长度

phi = 0.8 # AR(1) 系数

# ------------------------ 参数设定 -----------

epsilon = np.random.normal(0, 1, n) # 白噪声

ar1 = np.zeros(n)

for t in range(1, n):

ar1[t] = phi * ar1[t-1] + epsilon[t]

# 模拟单位根过程

unit_root = np.zeros(n)

for t in range(1, n):

unit_root[t] = unit_root[t-1] + epsilon[t]

# 绘图比较

plt.figure(figsize=(12, 6))

plt.plot(ar1, label="AR(1) Process (phi=0.8)", color="blue")

plt.plot(unit_root, label="Unit Root Process", color="red")

# 添加时间趋势线

time = np.arange(n)

ar1_trend = np.poly1d(np.polyfit(time, ar1, 1))(time)

unit_root_trend = np.poly1d(np.polyfit(time, unit_root, 1))(time)

# 绘图

plt.plot(time, ar1_trend, label="AR(1) Trend Line", color="cyan", linestyle="--")

plt.plot(time, unit_root_trend, label="Unit Root Trend Line", color="orange", linestyle="--")

plt.axhline(y=0, color="green", linestyle="--", alpha=0.5, label="y=0 Line")

plt.title("Comparison of AR(1) Process and Unit Root Process with Trend Lines", fontsize=16)

plt.xlabel("Time", fontsize=12)

plt.ylabel("Value", fontsize=12)

plt.legend()

plt.grid(True, linestyle="--", linewidth=0.5)

plt.tight_layout()

plt.show()

# 基本统计量

import pandas as pd

print("AR(1) Process Statistics:")

print(pd.Series(ar1).describe().round(2))

print("\nUnit Root Process Statistics:")

print(pd.Series(unit_root).describe().round(2))

AR(1) Process Statistics:

count 100.00

mean -0.52

std 1.44

min -3.65

25% -1.67

50% -0.50

75% 0.43

max 2.93

dtype: float64

Unit Root Process Statistics:

count 100.00

mean -6.90

std 4.64

min -12.74

25% -10.36

50% -8.77

75% -4.56

max 3.98

dtype: float64下图呈现了模拟 100 次的结果 (codes),发现 AR 过程的均值和方差是有限的,而单位根过程的均值虽然有限,但其方差会随着时间的推移不断增大,表现出非平稳的特征。

17.2 相关图和偏相关图

17.2.1 相关图 (ACF, Autocorrelation Function)

相关图展示了时间序列数据在不同滞后期的自相关系数。自相关系数衡量了当前值与过去值之间的线性关系,其定义公式为:

\[ \rho_k = \frac{\text{Cov}(X_t, X_{t-k})}{\sqrt{\text{Var}(X_t) \cdot \text{Var}(X_{t-k})}} \]

其中,\(k\) 表示滞后期,\(\text{Cov}\) 表示协方差,\(\text{Var}\) 表示方差。

17.2.2 偏相关图 (PACF, Partial Autocorrelation Function)

偏相关图展示了时间序列数据在不同滞后期的偏自相关系数。偏自相关系数衡量了当前值与某一滞后值之间的线性关系,剔除了其他中间滞后值的影响。其定义公式为:

\[ \phi_{kk} = \text{Partial Correlation}(X_t, X_{t-k} | X_{t-1}, X_{t-2}, \dots, X_{t-(k-1)}) \]

偏相关系数可以通过递归方法(如 Durbin-Levinson 算法)计算。

17.2.3 相关图和偏相关图的特征

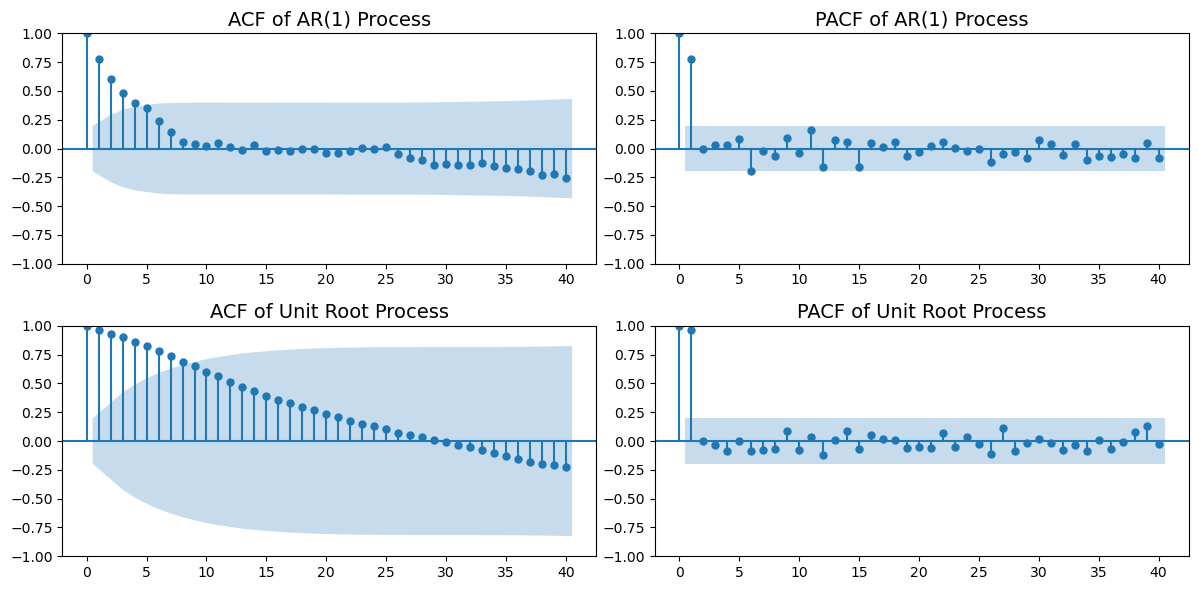

17.2.3.1 AR(p) 模型的相关图和偏相关图特征

- 相关图 (ACF):AR(p) 模型的自相关函数通常在滞后期 \(k > p\) 时呈指数衰减或振荡衰减。

- 偏相关图 (PACF):AR(p) 模型的偏自相关函数在滞后期 \(k > p\) 时迅速趋近于零,而在 \(k \leq p\) 时可能显著。

17.2.3.2 单位根过程的相关图特征

单位根过程(如随机游走)的相关图和偏相关图具有以下特征: - 相关图 (ACF):自相关函数在所有滞后期 \(k\) 上都接近于 1,且衰减非常缓慢。 - 偏相关图 (PACF):偏自相关函数在滞后期 \(k = 1\) 时显著,而在 \(k > 1\) 时迅速趋近于零。

这些特征反映了单位根过程的非平稳性和强记忆效应。

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

import matplotlib.pyplot as plt

# 绘制 AR(1) 过程的 ACF 和 PACF

plt.figure(figsize=(12, 6))

plt.subplot(2, 2, 1)

plot_acf(ar1, lags=40, ax=plt.gca())

plt.title('ACF of AR(1) Process', fontsize=14)

plt.subplot(2, 2, 2)

plot_pacf(ar1, lags=40, ax=plt.gca())

plt.title('PACF of AR(1) Process', fontsize=14)

# 绘制单位根过程的 ACF 和 PACF

plt.subplot(2, 2, 3)

plot_acf(unit_root, lags=40, ax=plt.gca())

plt.title('ACF of Unit Root Process', fontsize=14)

plt.subplot(2, 2, 4)

plot_pacf(unit_root, lags=40, ax=plt.gca())

plt.title('PACF of Unit Root Process', fontsize=14)

plt.tight_layout()

plt.show()

17.3 MA 过程

17.3.1 移动平均过程 (Moving Average Process)

移动平均过程 (MA) 是时间序列分析中的一种基本模型。它假设当前值是过去若干期随机扰动项的线性组合。MA 过程的数学表达式为:

\[ X_t = \mu + \epsilon_t + \theta_1 \epsilon_{t-1} + \theta_2 \epsilon_{t-2} + \dots + \theta_q \epsilon_{t-q} \tag{1} \]

其中: - \(X_t\) 是时间序列的当前值; - \(\mu\) 是序列的均值; - \(\epsilon_t\) 是白噪声项,满足 \(E[\epsilon_t] = 0\) 和 \(Var[\epsilon_t] = \sigma^2\); - \(\theta_1, \theta_2, \dots, \theta_q\) 是模型参数; - \(q\) 是移动平均过程的阶数。

17.3.2 MA(1) 模型

当 \(q=1\) 时,MA(1) 模型的形式为:

\[ X_t = \mu + \epsilon_t + \theta_1 \epsilon_{t-1} \tag{2} \]

在 MA(1) 模型中,当前值 \(X_t\) 由当前随机扰动 \(\epsilon_t\) 和前一期随机扰动 \(\epsilon_{t-1}\) 的加权和决定。

17.3.3 MA 过程的特性

- 平稳性:MA 过程是平稳的,因为它仅依赖于有限个随机扰动项。

- 自相关函数 (ACF):

- MA(q) 模型的自相关函数在滞后期 \(k > q\) 时为 0;

- 在滞后期 \(k \leq q\) 时,自相关函数可能显著。

- MA(q) 模型的自相关函数在滞后期 \(k > q\) 时为 0;

- 偏自相关函数 (PACF):

- MA(q) 模型的偏自相关函数在所有滞后期 \(k > 1\) 时迅速衰减;

- 在滞后期 \(k = 1\) 时,偏自相关函数可能显著。

- MA(q) 模型的偏自相关函数在所有滞后期 \(k > 1\) 时迅速衰减;

17.3.4 MA 过程的应用

MA 过程常用于建模时间序列中的短期依赖关系。例如: - 经济数据中的短期波动; - 金融数据中的短期价格变化。

17.3.5 AR 过程和 MA 过程的区别

AR 过程和 MA 过程是时间序列分析中的两种基本模型,它们在建模思路、平稳性、自相关函数和偏自相关函数等方面存在显著差异。以下是它们的主要区别: - 建模思路:AR 过程假设当前值与过去值之间存在线性关系,而 MA 过程假设当前值是过去随机扰动项的线性组合。 - 平稳性:AR 过程的平稳性取决于参数的取值,而 MA 过程是平稳的,因为它仅依赖于有限个随机扰动项。

17.3.5.1 AR(1) 可以表示为 MA(∞)

AR(1) 过程可以通过递归展开的方式表示为 MA(∞) 过程。具体来说,假设 AR(1) 模型为:

\[ X_t = \phi X_{t-1} + \epsilon_t \]

将 \(X_{t-1}\) 代入上述公式,可以得到:

\[ X_t = \phi (\phi X_{t-2} + \epsilon_{t-1}) + \epsilon_t = \phi^2 X_{t-2} + \phi \epsilon_{t-1} + \epsilon_t \]

继续递归下去,可以得到:

\[ X_t = \phi^t X_0 + \sum_{i=0}^{\infty} \phi^i \epsilon_{t-i} \]

由此可见,AR(1) 过程可以表示为一个 MA(∞) 过程,其中当前值 \(X_t\) 是所有过去随机扰动项 \(\epsilon_{t-i}\) 的加权和,权重由 \(\phi^i\) 决定,并随着 \(i\) 的增大呈指数衰减。

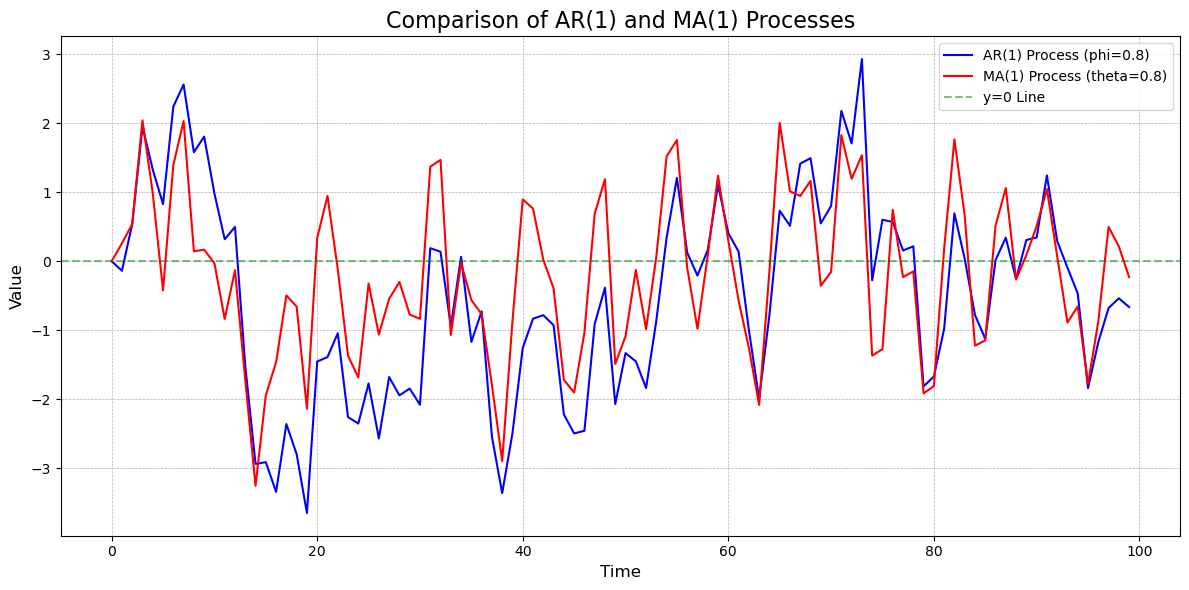

# 模拟分析:AR(1) 和 MA(1) 过程的差别

# 模拟 MA(1) 过程

theta = 0.8 # MA(1) 系数

ma1 = np.zeros(n)

for t in range(1, n):

ma1[t] = epsilon[t] + theta * epsilon[t-1]

# 绘图比较 AR(1) 和 MA(1) 过程

plt.figure(figsize=(12, 6))

plt.plot(ar1, label="AR(1) Process (phi=0.8)", color="blue")

plt.plot(ma1, label="MA(1) Process (theta=0.8)", color="red")

# 添加时间趋势线

plt.axhline(y=0, color="green", linestyle="--", alpha=0.5, label="y=0 Line")

plt.title("Comparison of AR(1) and MA(1) Processes", fontsize=16)

plt.xlabel("Time", fontsize=12)

plt.ylabel("Value", fontsize=12)

plt.legend()

plt.grid(True, linestyle="--", linewidth=0.5)

plt.tight_layout()

plt.show()

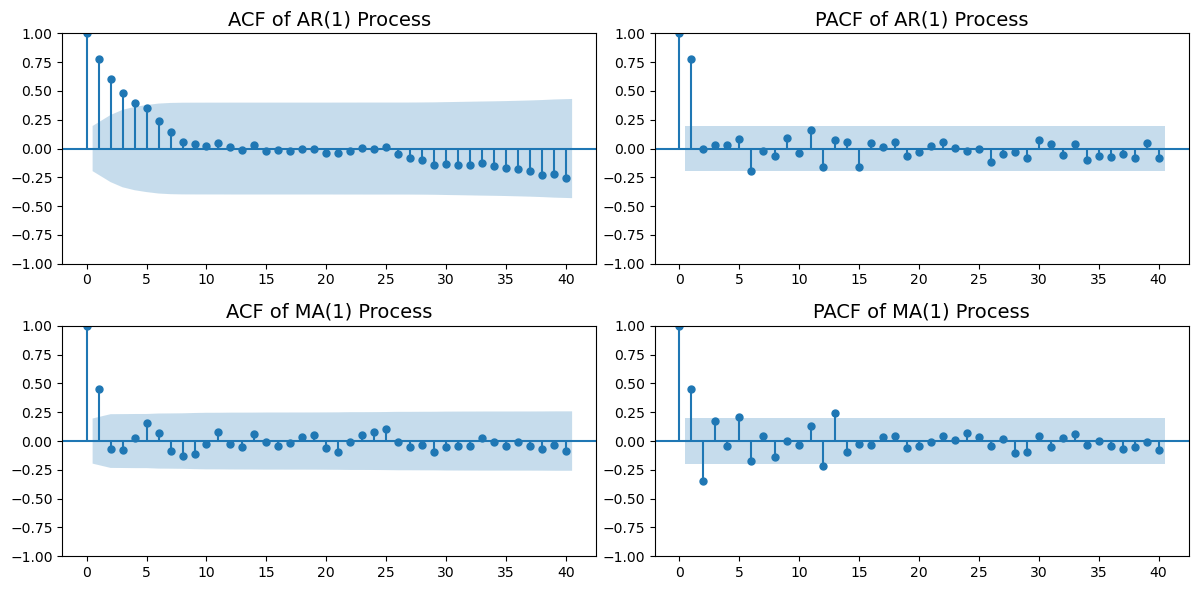

17.3.6 AR(1) 和 MA(1) 的区别:ACF 和 PACF

AR(1) 和 MA(1) 模型在自相关函数 (ACF) 和偏自相关函数 (PACF) 上有显著的区别。以下是它们的主要区别: - AR(1) 模型: - ACF:在滞后期 \(k > 1\) 时,ACF 呈指数衰减或振荡衰减; - PACF:在滞后期 \(k = 1\) 时显著,而在 \(k > 1\) 时迅速趋近于零。 - 这表明 AR(1) 模型具有长记忆效应,当前值与过去值之间存在较强的线性关系。 - MA(1) 模型: - ACF:在滞后期 \(k > 1\) 时迅速趋近于零; - PACF:在滞后期 \(k = 1\) 时显著,而在 \(k > 1\) 时迅速趋近于零。 - 这表明 MA(1) 模型具有短记忆效应,当前值主要受最近的随机扰动项影响。

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

# ACF 和 PACF 分析:AR(1) v.s. MA(1)

import matplotlib.pyplot as plt

# 绘制 AR(1) 过程的 ACF 和 PACF

plt.figure(figsize=(12, 6))

plt.subplot(2, 2, 1)

plot_acf(ar1, lags=40, ax=plt.gca())

plt.title('ACF of AR(1) Process', fontsize=14)

plt.subplot(2, 2, 2)

plot_pacf(ar1, lags=40, ax=plt.gca())

plt.title('PACF of AR(1) Process', fontsize=14)

# 绘制 MA(1) 过程的 ACF 和 PACF

plt.subplot(2, 2, 3)

plot_acf(ma1, lags=40, ax=plt.gca())

plt.title('ACF of MA(1) Process', fontsize=14)

plt.subplot(2, 2, 4)

plot_pacf(ma1, lags=40, ax=plt.gca())

plt.title('PACF of MA(1) Process', fontsize=14)

plt.tight_layout()

plt.show()

17.4 ARMA(p, q) 模型

ARMA 模型(AutoRegressive Moving Average Model,自回归移动平均模型)是时间序列分析中的一种经典模型。它结合了 AR(p) 模型和 MA(q) 模型的特性,用于描述时间序列数据的线性依赖结构。

ARMA(p, q) 模型的数学表达式为:

\[ X_t = \phi_1 X_{t-1} + \phi_2 X_{t-2} + \dots + \phi_p X_{t-p} + \epsilon_t + \theta_1 \epsilon_{t-1} + \theta_2 \epsilon_{t-2} + \dots + \theta_q \epsilon_{t-q} \]

其中: - \(X_t\) 是时间序列的当前值; - \(\phi_1, \phi_2, \dots, \phi_p\) 是 AR 部分的参数; - \(\theta_1, \theta_2, \dots, \theta_q\) 是 MA 部分的参数; - \(\epsilon_t\) 是白噪声项,满足 \(E[\epsilon_t] = 0\) 和 \(Var[\epsilon_t] = \sigma^2\); - \(p\) 是自回归部分的阶数; - \(q\) 是移动平均部分的阶数。

17.4.1 特性

- 平稳性:ARMA 模型要求时间序列是平稳的,即均值、方差和自相关函数在时间上保持不变。

- 自相关函数 (ACF) 和 偏自相关函数 (PACF):

- ARMA 模型的 ACF 和 PACF 通常在滞后期 \(k > \max(p, q)\) 时迅速衰减。

- ACF 和 PACF 的具体模式取决于 \(p\) 和 \(q\) 的值。

17.4.2 模型选择

在实际应用中,选择 ARMA 模型的阶数 \(p\) 和 \(q\) 通常需要结合以下方法: 1. ACF 和 PACF 图:通过观察时间序列的 ACF 和 PACF 图,初步判断 \(p\) 和 \(q\) 的可能值。 2. 信息准则:如 AIC(Akaike 信息准则)和 BIC(贝叶斯信息准则),用于选择最优的 \(p\) 和 \(q\)。 3. 模型拟合优度:通过比较不同模型的拟合效果,选择最优模型。

17.4.3 应用场景

ARMA 模型适用于平稳时间序列的建模和预测,常见的应用场景包括: - 经济数据(如 GDP、消费指数)的短期预测; - 金融数据(如股票价格、汇率)的波动分析; - 工业过程中的信号处理。

17.4.4 示例

在上文中,我们已经模拟了 AR(1) 和 MA(1) 过程,并绘制了它们的 ACF 和 PACF 图。接下来,我们可以尝试拟合 ARMA 模型来描述这些时间序列的特性。

以下是拟合 ARMA 模型的步骤: 1. 检查时间序列的平稳性(如 ADF 检验)。 2. 绘制 ACF 和 PACF 图,初步判断 \(p\) 和 \(q\) 的值。 3. 使用 statsmodels 库中的 ARIMA 模块拟合 ARMA 模型。 4. 检查模型的残差是否为白噪声。 5. 使用模型进行预测。

通过 ARMA 模型,我们可以更好地理解时间序列的动态特性,并进行有效的预测。

17.4.5 注意

多数情况下,使用 ARMA(1,1) 模型就可以描述多数平稳时间序列的特征:

\[ X_t = \phi_1 X_{t-1} + \theta_1 \epsilon_{t-1} + \epsilon_t \]

17.5 单位根检验

从上面的 \(ARMA(1,1)\) 模型的结果来看,\(AR(1)\) 系数的估计值为 \(0.9847\),接近于 \(1\),这表明该序列可能是一个单位根序列。

我们可以使用 statsmodels 库中的 adfuller 函数来进行单位根检验。

17.5.1 ADF 检验

给定一个时间序列 \(X_t\),我们可以使用以下的 ADF 检验来检验 \(X_t\) 是否是平稳的: \[ X_t = \phi_0 + \phi_1 X_{t-1} + \phi_2 X_{t-2} + ... + \phi_p X_{t-p} + \epsilon_t\] 其中,\(\epsilon_t\) 是一个白噪声序列。

ADF 检验的原假设是:\(X_t\) 是一个单位根序列,即 \(H_0: \phi_1 = 1\)。 如果 \(H_0\) 被拒绝,则说明 \(X_t\) 是平稳的。

ADF 检验包含几种典型的数据生成机制: - 纯随机游走:\(X_t = X_{t-1} + \epsilon_t\),其中 \(\epsilon_t\) 是一个白噪声序列。 - 随机游走加趋势:\(X_t = \phi_0 + \phi_1 X_{t-1} + \phi_2 t + \epsilon_t\),其中 \(\epsilon_t\) 是一个白噪声序列,\(t\) 是时间趋势项。 - 随机游走加季节性:\(X_t = \phi_0 + \phi_1 X_{t-1} + S_t + \epsilon_t\),其中 \(\epsilon_t\) 是一个白噪声序列,\(S_t\) 是季节性项。 - 随机游走加趋势和季节性:\(X_t = \phi_0 + \phi_1 X_{t-1} + \phi_2 t + S_t + \epsilon_t\),其中 \(\epsilon_t\) 是一个白噪声序列,\(t\) 是时间趋势项,\(S_t\) 是季节性项。

17.5.2 其它检验方法

除了 ADF 检验,还有其他一些常用的单位根检验方法,如 KPSS 检验和 PP 检验。

17.5.2.1 KPSS 检验

KPSS 检验的原假设是:\(X_t\) 是平稳的,即 \(H_0: \phi_1 < 1\)。 如果 \(H_0\) 被拒绝,则说明 \(X_t\) 是一个单位根序列。

17.5.2.2 PP 检验

PP 检验的原假设是:\(X_t\) 是一个单位根序列,即 \(H_0: \phi_1 = 1\)。 如果 \(H_0\) 被拒绝,则说明 \(X_t\) 是平稳的。

17.5.3 模拟分析

我们生成四个不同的时间序列,分别是 AR(1)、带时间趋势的 AR(1)、ARMA(1,1) 和单位根过程。以下是它们的生成过程:

AR(1) 平稳序列

AR(1) 模型的数学表达式为:

\[ X_t = \phi X_{t-1} + \epsilon_t \]

其中,\(\phi = 0.8\),\(\epsilon_t\) 是均值为 0、方差为 1 的白噪声。带时间趋势的 AR(1) 序列

在 AR(1) 模型的基础上加入线性时间趋势:

\[ X_t = \phi X_{t-1} + \epsilon_t + \text{trend}(t) \]

其中,\(\text{trend}(t)\) 是一个线性增长的时间趋势项。ARMA(1,1) 平稳序列

ARMA(1,1) 模型的数学表达式为:

\[ X_t = \phi X_{t-1} + \epsilon_t + \theta \epsilon_{t-1} \]

其中,\(\phi = 0.8\),\(\theta = 0.5\),\(\epsilon_t\) 是均值为 0、方差为 1 的白噪声。单位根过程

单位根过程的数学表达式为:

\[ X_t = X_{t-1} + \epsilon_t \]

其中,\(\epsilon_t\) 是均值为 0、方差为 1 的白噪声。

通过这些序列的生成,我们可以观察不同时间序列的特性,并进行单位根检验和其他分析。

import statsmodels.api as sm

from statsmodels.tsa.stattools import adfuller

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

# 模拟四个序列

np.random.seed(42)

n = 200 # 时间序列长度

epsilon = np.random.normal(0, 1, n)

# 1. AR(1) 平稳

phi = 0.8

ar1_stationary = np.zeros(n)

for t in range(1, n):

ar1_stationary[t] = phi * ar1_stationary[t-1] + epsilon[t]

# 2. AR(1) + 时间趋势

trend = np.linspace(0, 10, n)

ar1_with_trend = np.zeros(n)

for t in range(1, n):

ar1_with_trend[t] = phi * ar1_with_trend[t-1] + epsilon[t]

ar1_with_trend += trend

# 3. ARMA(1,1) 平稳

theta = 0.5

arma11_stationary = np.zeros(n)

for t in range(1, n):

arma11_stationary[t] = phi * arma11_stationary[t-1] + epsilon[t] + theta * epsilon[t-1]

# 4. 单位根过程

unit_root = np.zeros(n)

for t in range(1, n):

unit_root[t] = unit_root[t-1] + epsilon[t]17.5.3.1 图形比较

我们先直观地展示这四个序列的图形,然后再分析其 ACF 和 PACF 图,最后通过单位根检验来验证它们的平稳性。

# 绘图比较

plt.figure(figsize=(12, 8))

# AR(1) 平稳序列

plt.subplot(2, 2, 1)

plt.plot(ar1_stationary, label="AR(1) Stationary", color="blue")

plt.title("AR(1) Stationary Sequence", fontsize=14)

plt.xlabel("Time", fontsize=12)

plt.ylabel("Value", fontsize=12)

plt.legend()

plt.grid(True, linestyle="--", linewidth=0.5)

# AR(1) + 时间趋势序列

plt.subplot(2, 2, 2)

plt.plot(ar1_with_trend, label="AR(1) with Trend", color="orange")

plt.title("AR(1) with Trend Sequence", fontsize=14)

plt.xlabel("Time", fontsize=12)

plt.ylabel("Value", fontsize=12)

plt.legend()

plt.grid(True, linestyle="--", linewidth=0.5)

# ARMA(1,1) 平稳序列

plt.subplot(2, 2, 3)

plt.plot(arma11_stationary, label="ARMA(1,1) Stationary", color="green")

plt.title("ARMA(1,1) Stationary Sequence", fontsize=14)

plt.xlabel("Time", fontsize=12)

plt.ylabel("Value", fontsize=12)

plt.legend()

plt.grid(True, linestyle="--", linewidth=0.5)

# 单位根过程

plt.subplot(2, 2, 4)

plt.plot(unit_root, label="Unit Root Process", color="red")

plt.title("Unit Root Process", fontsize=14)

plt.xlabel("Time", fontsize=12)

plt.ylabel("Value", fontsize=12)

plt.legend()

plt.grid(True, linestyle="--", linewidth=0.5)

plt.tight_layout()

plt.show()

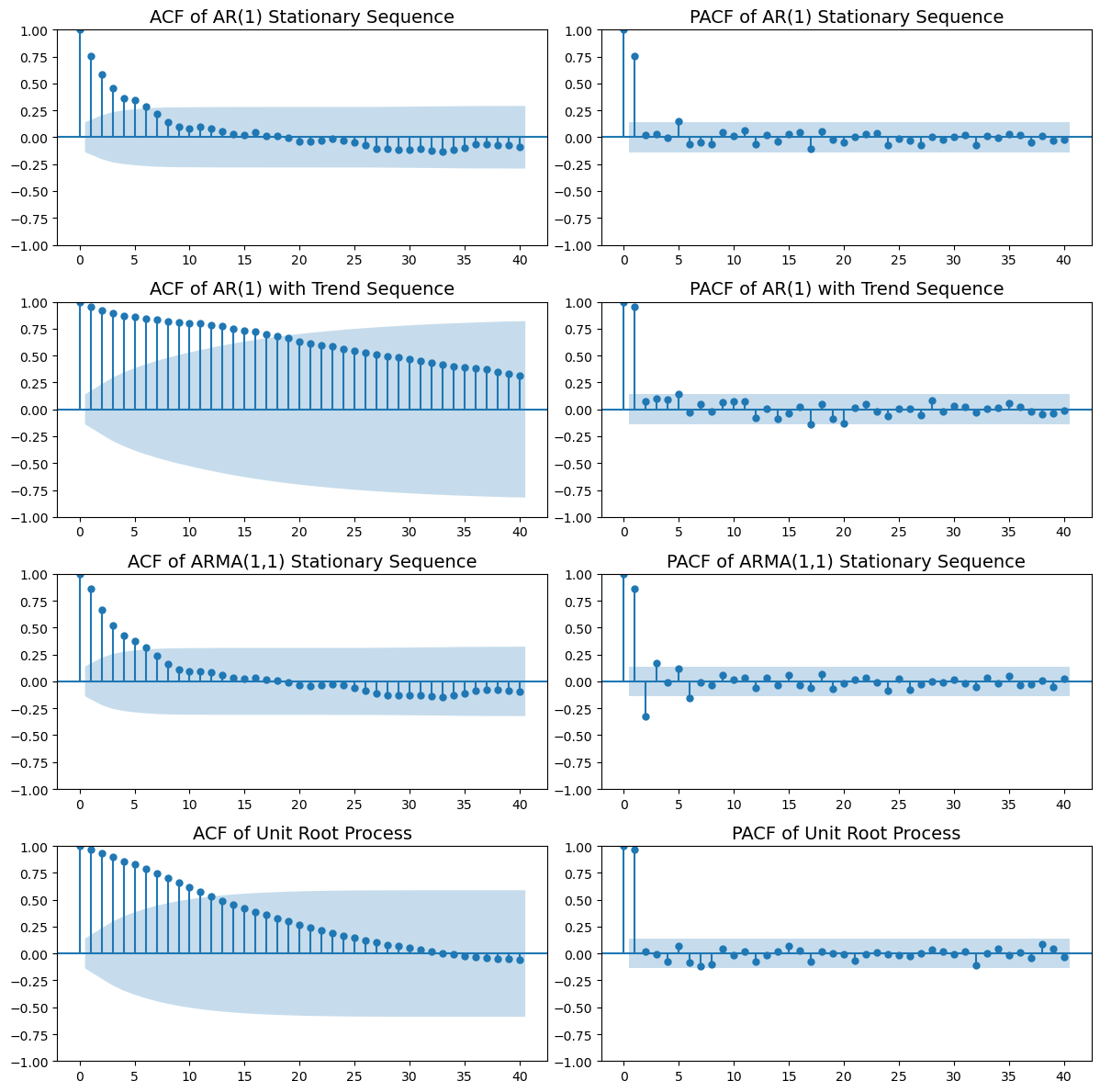

17.5.3.2 ACF 和 PACF 图

我们可以使用 statsmodels 库中的 plot_acf 和 plot_pacf 函数来绘制 ACF 和 PACF 图。以下是对四个序列的 ACF 和 PACF 图的分析:

# 绘制 ACF 和 PACF 图

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

plt.figure(figsize=(12, 12))

# AR(1) 平稳序列

plt.subplot(4, 2, 1)

plot_acf(ar1_stationary, lags=40, ax=plt.gca())

plt.title('ACF of AR(1) Stationary Sequence', fontsize=14)

plt.subplot(4, 2, 2)

plot_pacf(ar1_stationary, lags=40, ax=plt.gca())

plt.title('PACF of AR(1) Stationary Sequence', fontsize=14)

# AR(1) + 时间趋势序列

plt.subplot(4, 2, 3)

plot_acf(ar1_with_trend, lags=40, ax=plt.gca())

plt.title('ACF of AR(1) with Trend Sequence', fontsize=14)

plt.subplot(4, 2, 4)

plot_pacf(ar1_with_trend, lags=40, ax=plt.gca())

plt.title('PACF of AR(1) with Trend Sequence', fontsize=14)

# ARMA(1,1) 平稳序列

plt.subplot(4, 2, 5)

plot_acf(arma11_stationary, lags=40, ax=plt.gca())

plt.title('ACF of ARMA(1,1) Stationary Sequence', fontsize=14)

plt.subplot(4, 2, 6)

plot_pacf(arma11_stationary, lags=40, ax=plt.gca())

plt.title('PACF of ARMA(1,1) Stationary Sequence', fontsize=14)

# 单位根过程

plt.subplot(4, 2, 7)

plot_acf(unit_root, lags=40, ax=plt.gca())

plt.title('ACF of Unit Root Process', fontsize=14)

plt.subplot(4, 2, 8)

plot_pacf(unit_root, lags=40, ax=plt.gca())

plt.title('PACF of Unit Root Process', fontsize=14)

plt.tight_layout()

plt.show()

17.5.4 单位根检验

我们可以使用 statsmodels 库中的 adfuller 函数来进行单位根检验。以下是对四个序列的单位根检验结果的分析:

# 定义 test_stationarity 函数

def test_stationarity(timeseries):

# 进行ADF检验

adf_result = adfuller(timeseries)

print(f'ADF Statistic: {adf_result[0]}')

print(f'p-value: {adf_result[1]}')

if adf_result[1] <= 0.05:

print("Reject the null hypothesis: The time series is stationary.")

else:

print("Fail to reject the null hypothesis: The time series is non-stationary.")

# 进行KPSS检验

from statsmodels.tsa.stattools import kpss

kpss_result = kpss(timeseries, regression='c')

print(f'KPSS Statistic: {kpss_result[0]}')

print(f'p-value: {kpss_result[1]}')

if kpss_result[1] <= 0.05:

print("Reject the null hypothesis: The time series is non-stationary.")

else:

print("Fail to reject the null hypothesis: The time series is stationary.")

# 执行单位根检验

print("AR(1) 平稳序列:")

test_stationarity(ar1_stationary)

print("\nAR(1) + 时间趋势序列:")

test_stationarity(ar1_with_trend)

print("\nARMA(1,1) 平稳序列:")

test_stationarity(arma11_stationary)

print("\n单位根序列:")

test_stationarity(unit_root)AR(1) 平稳序列:

ADF Statistic: -5.140188092198668

p-value: 1.1632040113030607e-05

Reject the null hypothesis: The time series is stationary.

KPSS Statistic: 0.40971623118293043

p-value: 0.0729671417314955

Fail to reject the null hypothesis: The time series is stationary.

AR(1) + 时间趋势序列:

ADF Statistic: -1.083734015465617

p-value: 0.7215148114561589

Fail to reject the null hypothesis: The time series is non-stationary.

KPSS Statistic: 1.9346683267076523

p-value: 0.01

Reject the null hypothesis: The time series is non-stationary.

ARMA(1,1) 平稳序列:

ADF Statistic: -3.6707270981703113

p-value: 0.004544260482266915

Reject the null hypothesis: The time series is stationary.

KPSS Statistic: 0.40642058881067256

p-value: 0.07438767723677908

Fail to reject the null hypothesis: The time series is stationary.

单位根序列:

ADF Statistic: -2.3072851790645252

p-value: 0.1696291207894372

Fail to reject the null hypothesis: The time series is non-stationary.

KPSS Statistic: 0.7001396636588889

p-value: 0.013532757849191916

Reject the null hypothesis: The time series is non-stationary.C:\Users\arlio\AppData\Local\Temp\ipykernel_4892\3041600984.py:14: InterpolationWarning: The test statistic is outside of the range of p-values available in the

look-up table. The actual p-value is smaller than the p-value returned.

kpss_result = kpss(timeseries, regression='c')17.6 待更新

# 3. VAR模型

def fit_var_model(data, maxlags=15):

model = VAR(data)

results = model.fit(maxlags=maxlags, ic='aic')

print(results.summary())

return results

# 4. Granger因果关系检验

def granger_causality_test(data, max_lag=15):

test_result = grangercausalitytests(data, max_lag, verbose=True)

return test_result

# 5. 协整检验

def cointegration_test(data):

score, p_value, _ = coint(data.iloc[:, 0], data.iloc[:, 1])

print(f'Cointegration test statistic: {score}')

print(f'p-value: {p_value}')

if p_value <= 0.05:

print("Reject the null hypothesis: The time series are cointegrated.")

else:

print("Fail to reject the null hypothesis: The time series are not cointegrated.")

# 6. VAR模型的脉冲响应函数

def impulse_response_function(model, steps=10):

irf = model.irf(steps)

irf.plot(orth=False)

plt.show()

# 7. VAR模型的方差分解

def variance_decomposition(model, steps=10):

fevd = model.fevd(steps)

fevd.plot()

plt.show()

# 8. VAR模型的预测

def forecast_var_model(model, steps=10):

forecast = model.forecast(model.y, steps=steps)

forecast_df = pd.DataFrame(forecast, index=pd.date_range(start=df_unemp.index[-1] + pd.DateOffset(1), periods=steps, freq='M'), columns=model.names)

return forecast_df